Telecommunications (Telcos) are increasingly dabbling in the insurance space, and this is enabled by the rise of the platform business model. Alike to the familiar brands you know like Netflix, Amazon, Facebook and Apple, the platform is basically any type of digital platform that creates value by connecting dispersed networks of individuals.

Within this platform economy, there is a triangular relationship between 3 parties, namely: (1) the platform (Telco); (2) the service provider (Insurer); (3) the Telco customer.

Say for Telcos, they are best positioned to harness and create large, scalable networks of users and resources that can be accessed by other service providers. Beyond providing connectivity, their assets and data can help support emerging offerings in the digital economy.

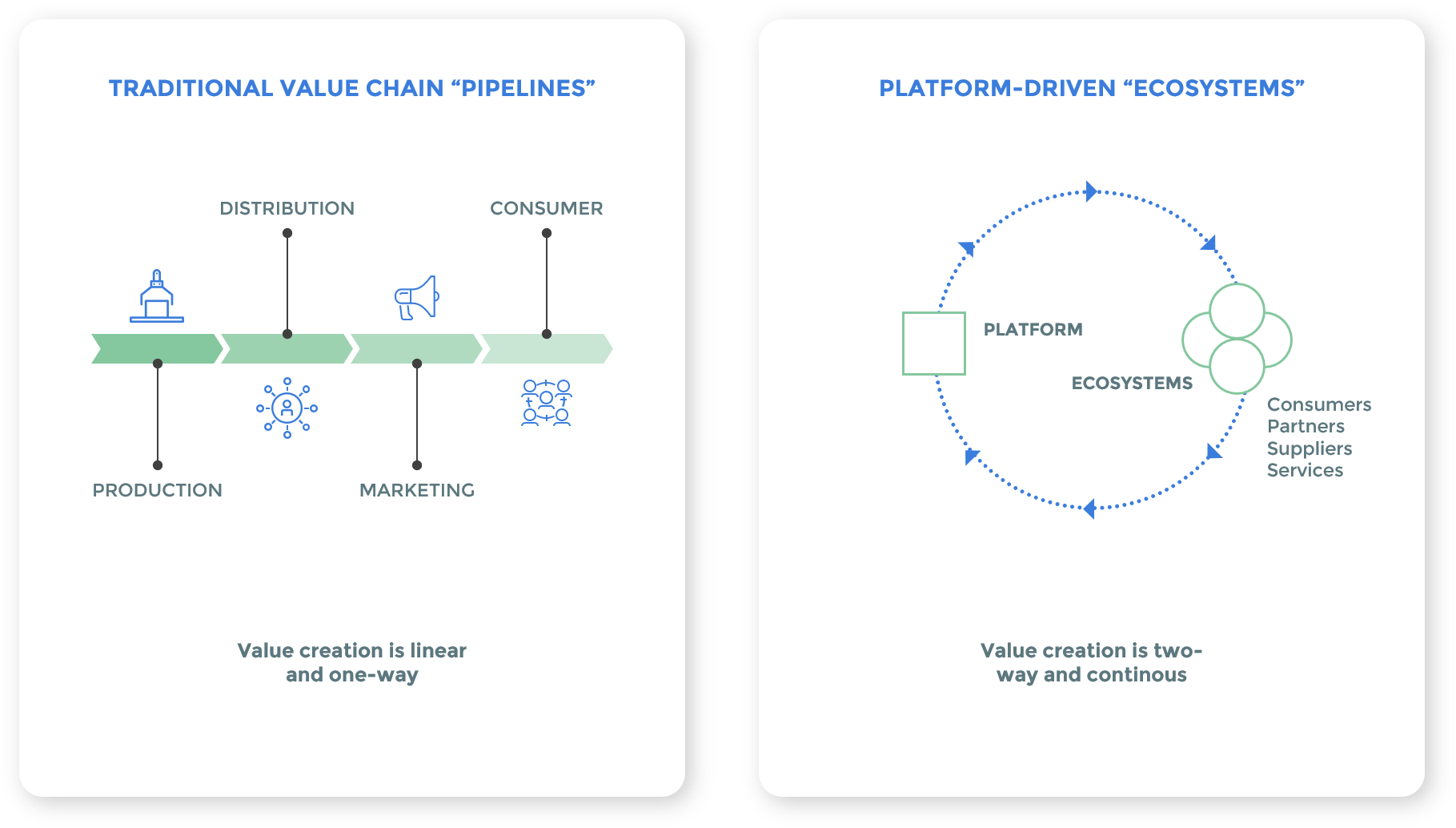

Pipeline Business Model vs. Platform Business Model (Source: The Guides Manifesto, Scott Annan)

Data is at the heart of telco-insurer partnerships.

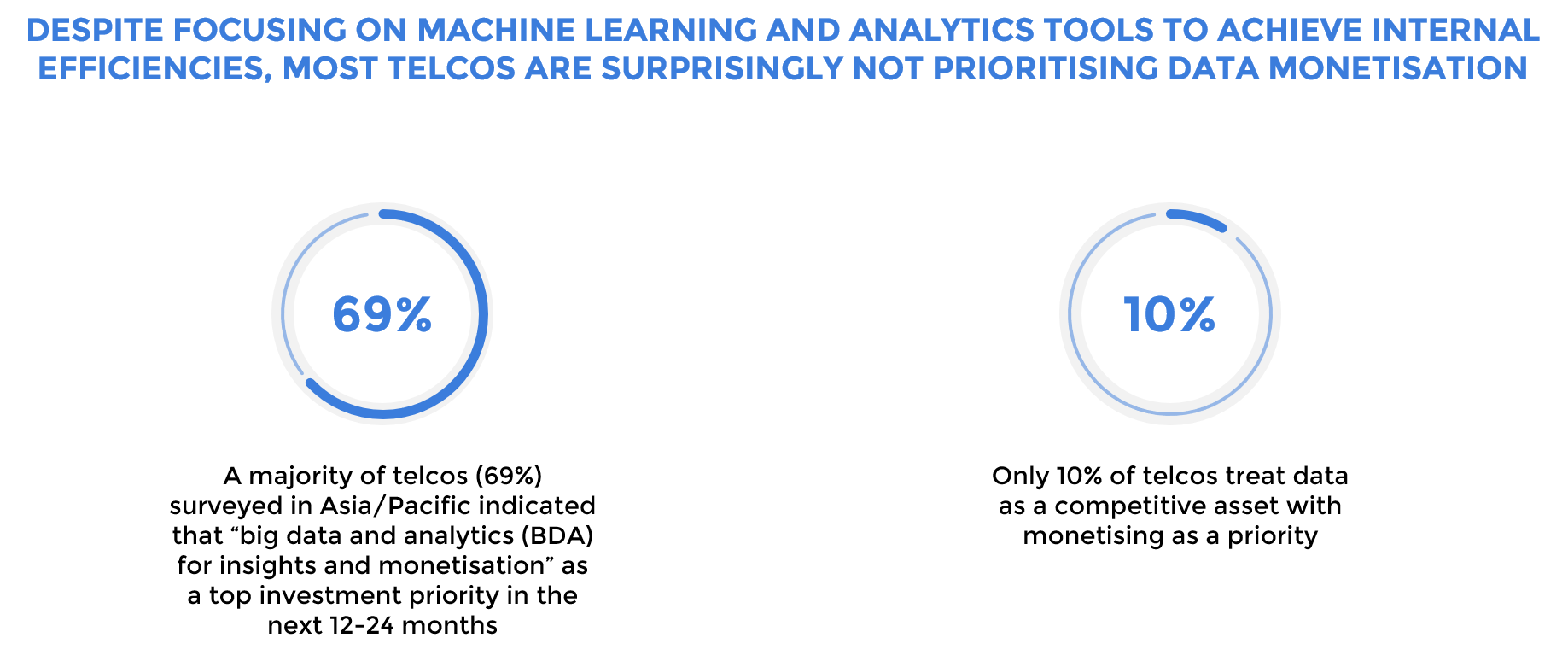

Untapped opportunities for data monetization (Source: New data monetisation opportunities for telcos in Asia, FUTURECIO)

1. Telcos can support insurers in their individual customer knowledge and authentication. The AI algorithm can be optimised to provide services like targeted pricing, optimized credit scoring, and risk management based on mobile telecommunications and sales data.

On the customer’s side of things, they also stand to benefit as the telco platforms can be optimised to ease their journey of signing up for a new service account, authenticate ATM withdrawals, or validate their identity when making purchases.

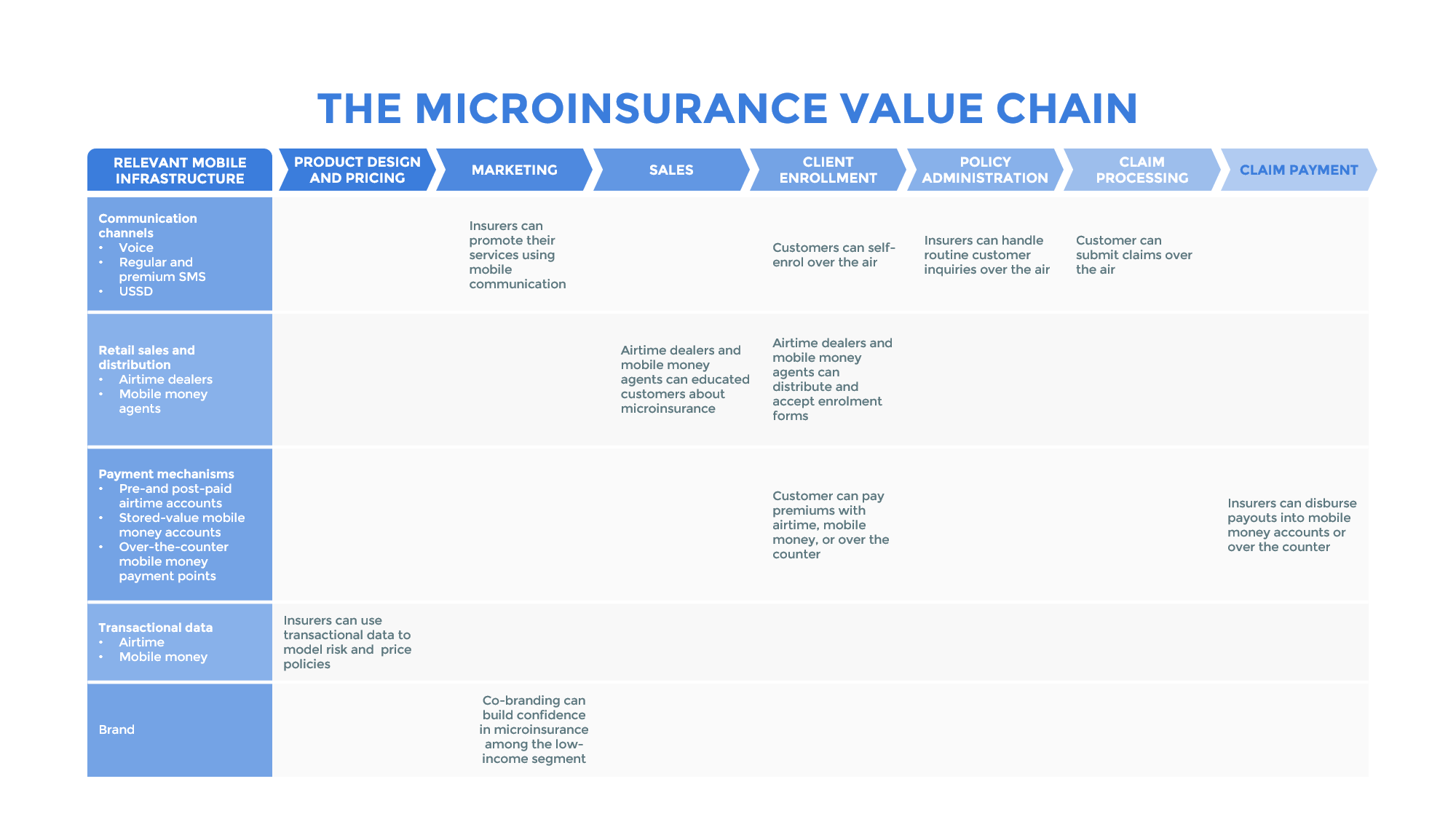

2. Telcos are powerful marketers for your product. Consider the communication channels they own and how you can leverage upon these to promote and sell insurance, enroll clients, and administer claims and payouts. Some of these channels include voice, text, USSD commands, and their mobile app.

Loyalty programmes also play a key role in the telco’s marketing strategy, and even this can be tapped on as there are instances of partnerships with insurers to provide their long-term customers with insurance under certain conditions. Beyond platforms, it’s possible that telcos may become your customers as well.

3. The rise of data privacy regulations has made it even more important for insurers to partner with services related to databases like telcos. Of course it’s possible for insurers to provide their services in isolation, but you have the potential to reach greater heights when connecting with elements in the digital ecosystem that deals with data.

Imagine the new insurance offerings that could have sprouted from customer profiles that come out of aggregated, anonymized data provided by telcos. Telcos have access to consumer’s behavior and retailing data on where and how to position advertising to maximize commercial effectiveness.

| What kinds of telco insurance (partnership)? | What is it? | Who is involved? |

| Telco-centric insurance | Covers broadband expenses and home contents (renovation, furniture, appliances, valuables and personal effects) in the event of disruption of services due to a fire or other types of damage. | Singtel and Great Eastern. |

| Mobile notification on insurance updates | Using blockchain and mobile notifications to deliver updates on insurance to customers via their phone. Insurers will match customer information to their mobile subscription information, and get their consent to opt-in. |

KT Corp and KB Insurance. |

| Mobile-based life microinsurance |

Customers can apply, subscribe and manage their life microinsurance plans entirely via their mobile phones and at low cost. | Sun Life Malaysia and U Mobile; Chubb and U Mobile. |

| Usage-based insurance | Insurers leverage on telco’s vehicle tracking solution/telematics technology to come up with an auto insurance offer for its users. | Etiqa Insurance, Takaful and Maxis. |

| COVID-19-targeted insurance | COVID-19 protection, in the form of partially-paid medical expenses and cash, for customers and loyalty members. | FWD Hong Kong and Hong Kong Telecom. |

| Telemedicine services | Covers medical expenses for consultation and medications delivered through the telco’s telemedicine platform. | FWD, Union |

| Digital payments for insurance | In developing countries, these partnerships allow rural citizens to access services in local health centres by making insurance payments by phone, using a digital wallet and with no need for a bank account. | AXA Mansard and Airtel. |

As of 2021, there are 4.66 billion active internet users worldwide – 59.5% of the global population. Of this total, 92.6% are accessing it via mobile devices. That said, mobile-enabled microinsurance can possibly leapfrog traditional insurance models by reaching the under-insured.

This is coupled with other growth drivers such as the rise of the gig economy, and appealing to the likes of millennials and the ‘digital native’ generation which are expecting greater efficiency and personalization in the delivery of insurance.

Scale is king in insurance and those who have partnered with telcos have reached scale quickly. Also, the incredibly diverse telco-insurer partnerships as seen in the table above reflects that insurers are coming up with progressively sophisticated offerings that combine a range of existing products such as life, personal accident, and hospital insurance.

This in tandem with taking advantage of the mobile phone allows insurers to reach their customers faster and cheaper.

Ways that Insurers can Leverage on Telcos (Source: Mobile Money for the Unbanked)

For now, it remains as an added value for telcos to support their core business. But it’s only a matter of time before they see it as their share of pie to take. That being said, this means insurers will constantly need to be on the lookout for new partnerships and think really hard about reinventing their offerings and processes.